Coincidentally, myself and two of my staff had to find new insurers in the last six months. Not for having solar panels, just companies reducing exposure in FL.

I had a new roof put on last March, but I found the insurers different excuses to cancel policies interesting:

Homeowners adding solar panels study energy savings and break-even costs, but they should also call their insurer: Some increase premiums and some cancel policies.

FORT LAUDERDALE, Fla. – As electric bills surge and the federal government offers generous tax incentives for renewable energy investments, more and more Florida homeowners are seriously considering rooftop solar systems.

But in calculating system costs vs. electric bill savings, many would-be solar owners are neglecting to consider how a solar system will affect their home insurance bill – or how difficult it might be to find a company that will insure them at all.

And with insurance premiums skyrocketing for all Florida homeowners, solar customers who can obtain coverage might also find that the price increase will wipe out any energy-cost savings they expected from going solar.

“It’s a big deal and a lot of folks don’t realize that many carriers don’t accept solar panels,” says Dulce Suarez-Resnick, vice president at the Miami-based agency Acentria Insurance.

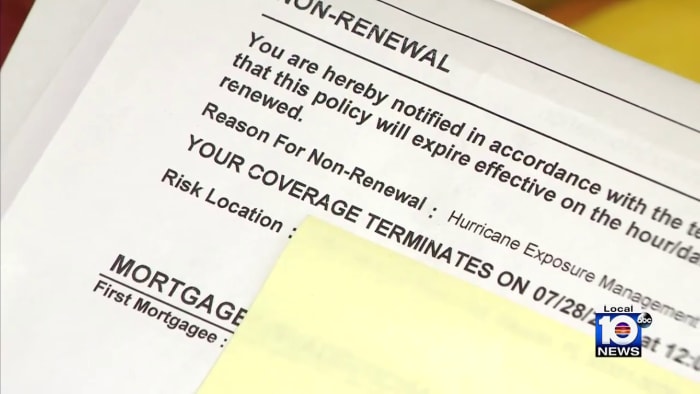

Oakland Park homeowner Holy Strawbridge learned this the hard way. She installed a modest 8,000 kilowatt system atop her home about two years ago and recently signed up for coverage with Edison Insurance Company. After the insurer sent an inspector to her home, she received a letter canceling her entire policy.

“I was shocked,” Strawbridge said. “I’ve never filed an insurance claim and I’ve lived in this house since 2001.”

The reasons cited in the cancellation letter sent by Edison: Her solar panels are ineligible for coverage due to the age of her roof (11 years) and because she has a tile roof.

Those aren’t the only reasons insurers won’t cover rooftop solar systems, according to interviews with solar installers, solar energy advocates, and insurance agents. Insurers who do business in Florida offer a wide variety of reasons for refusing to insure homes with them.

Florida Power & Light’s net metering contract requires homeowners to take responsibility for all potential damages, says Ryan Papy, president of Palmetto Bay-based Keyes Insurance. “So if there’s a surge running through your panels that causes damage to the grid or other homes, the client is responsible.”

Solar installers and advocates call that justification unfounded. They say all equipment used to connect rooftop solar systems to the grid comply with state building and electrical codes and are inspected by utilities before new systems are activated. Utilities also have authority to come onto solar owners’ properties and disconnect them if they suspect any safety issues, they say.

Solar advocates wonder if the net metering concerns are just excuse insurers are giving to justify dropping customers.

Many insurers who operate in Florida, faced with mounting losses, have been dropping or nonrenewing policies to reduce the amount of overall risk they carry on their books of business. In some cases, state insurance regulators have ordered insurers to shed policies so they can afford to purchase reinsurance – insurance that insurers must carry to be able to pay all claims after a catastrophe.

Justin Hoysradt, president of Vinyasun, a solar installation company based in West Palm Beach, says the potential dangers of backfeeding are exaggerated. Since 2006, all power-producing inverters have complied with an electrical standard called U.L. 1741, Hoysradt said. This standard requires solar system inverters to be able to detect utility outages or any odd voltage disruption and automatically disconnect the solar systems from the grid.

Hoysradt says he is unaware of any documented instance of injury or damage from a properly installed UL 1741-certified inverter. The cut-off technology is so dependable that utilities recently removed a requirement that solar systems be equipped with separate redundant manual lockable disconnects, he said.

Until about a year ago, Hoysradt rarely heard customers complain that they couldn’t find or keep insurance because of their solar systems. Now, at least one potential customer a day says their insurer could not guarantee they wouldn’t be dropped if they install solar, he said.

Other insurers have told homeowners that net metering turns them into commercial utilities and they are no longer eligible for homeowner insurance policies, said Heaven Campbell, Florida program directors for Solar United Neighbors, a nationwide nonprofit that helps solar customers form co-ops to secure better pricing. Campbell says her organization has documented about 60 homeowner complaints over the past year. They either say they’ve been cancelled after installing solar panels or told they would no longer be eligible for coverage if they install panels, she said.

I had a new roof put on last March, but I found the insurers different excuses to cancel policies interesting:

Homeowners adding solar panels study energy savings and break-even costs, but they should also call their insurer: Some increase premiums and some cancel policies.

FORT LAUDERDALE, Fla. – As electric bills surge and the federal government offers generous tax incentives for renewable energy investments, more and more Florida homeowners are seriously considering rooftop solar systems.

But in calculating system costs vs. electric bill savings, many would-be solar owners are neglecting to consider how a solar system will affect their home insurance bill – or how difficult it might be to find a company that will insure them at all.

And with insurance premiums skyrocketing for all Florida homeowners, solar customers who can obtain coverage might also find that the price increase will wipe out any energy-cost savings they expected from going solar.

“It’s a big deal and a lot of folks don’t realize that many carriers don’t accept solar panels,” says Dulce Suarez-Resnick, vice president at the Miami-based agency Acentria Insurance.

Oakland Park homeowner Holy Strawbridge learned this the hard way. She installed a modest 8,000 kilowatt system atop her home about two years ago and recently signed up for coverage with Edison Insurance Company. After the insurer sent an inspector to her home, she received a letter canceling her entire policy.

“I was shocked,” Strawbridge said. “I’ve never filed an insurance claim and I’ve lived in this house since 2001.”

The reasons cited in the cancellation letter sent by Edison: Her solar panels are ineligible for coverage due to the age of her roof (11 years) and because she has a tile roof.

Those aren’t the only reasons insurers won’t cover rooftop solar systems, according to interviews with solar installers, solar energy advocates, and insurance agents. Insurers who do business in Florida offer a wide variety of reasons for refusing to insure homes with them.

Net metering flagged by insurers

Increasingly, insurers are claiming that solar systems with net metering connections to utilities – which is virtually all of them in Florida – pose a unique risk of injury to line workers and damage to the utility grid.Florida Power & Light’s net metering contract requires homeowners to take responsibility for all potential damages, says Ryan Papy, president of Palmetto Bay-based Keyes Insurance. “So if there’s a surge running through your panels that causes damage to the grid or other homes, the client is responsible.”

Solar installers and advocates call that justification unfounded. They say all equipment used to connect rooftop solar systems to the grid comply with state building and electrical codes and are inspected by utilities before new systems are activated. Utilities also have authority to come onto solar owners’ properties and disconnect them if they suspect any safety issues, they say.

Solar advocates wonder if the net metering concerns are just excuse insurers are giving to justify dropping customers.

Many insurers who operate in Florida, faced with mounting losses, have been dropping or nonrenewing policies to reduce the amount of overall risk they carry on their books of business. In some cases, state insurance regulators have ordered insurers to shed policies so they can afford to purchase reinsurance – insurance that insurers must carry to be able to pay all claims after a catastrophe.

Justin Hoysradt, president of Vinyasun, a solar installation company based in West Palm Beach, says the potential dangers of backfeeding are exaggerated. Since 2006, all power-producing inverters have complied with an electrical standard called U.L. 1741, Hoysradt said. This standard requires solar system inverters to be able to detect utility outages or any odd voltage disruption and automatically disconnect the solar systems from the grid.

Hoysradt says he is unaware of any documented instance of injury or damage from a properly installed UL 1741-certified inverter. The cut-off technology is so dependable that utilities recently removed a requirement that solar systems be equipped with separate redundant manual lockable disconnects, he said.

Until about a year ago, Hoysradt rarely heard customers complain that they couldn’t find or keep insurance because of their solar systems. Now, at least one potential customer a day says their insurer could not guarantee they wouldn’t be dropped if they install solar, he said.

Other insurers have told homeowners that net metering turns them into commercial utilities and they are no longer eligible for homeowner insurance policies, said Heaven Campbell, Florida program directors for Solar United Neighbors, a nationwide nonprofit that helps solar customers form co-ops to secure better pricing. Campbell says her organization has documented about 60 homeowner complaints over the past year. They either say they’ve been cancelled after installing solar panels or told they would no longer be eligible for coverage if they install panels, she said.