Because at our core we aren’t socialists or communists.A majority of the US citizenry does not fundamentally value long term planning and actions that benefit all of society.

Colleges

- AAC

- ACC

- Big 12

- Big East

- Big Ten

- Pac-12

- SEC

- Atlantic 10

- Conference USA

- Independents

- Junior College

- Mountain West

- Sun Belt

- MAC

- More

- Navy

- UAB

- Tulsa

- UTSA

- Charlotte

- Florida Atlantic

- Temple

- Rice

- East Carolina

- USF

- SMU

- North Texas

- Tulane

- Memphis

- Miami

- Louisville

- Virginia

- Syracuse

- Wake Forest

- Duke

- Boston College

- Virginia Tech

- Georgia Tech

- Pittsburgh

- North Carolina

- North Carolina State

- Clemson

- Florida State

- Cincinnati

- BYU

- Houston

- Iowa State

- Kansas State

- Kansas

- Texas

- Oklahoma State

- TCU

- Texas Tech

- Baylor

- Oklahoma

- UCF

- West Virginia

- Wisconsin

- Penn State

- Ohio State

- Purdue

- Minnesota

- Iowa

- Nebraska

- Illinois

- Indiana

- Rutgers

- Michigan State

- Maryland

- Michigan

- Northwestern

- Arizona State

- Oregon State

- UCLA

- Colorado

- Stanford

- Oregon

- Arizona

- California

- Washington

- USC

- Utah

- Washington State

- Texas A&M

- Auburn

- Mississippi State

- Kentucky

- South Carolina

- Arkansas

- Florida

- Missouri

- Ole Miss

- Alabama

- LSU

- Georgia

- Vanderbilt

- Tennessee

- Louisiana Tech

- New Mexico State

- Middle Tennessee

- Western Kentucky

- UTEP

- Florida International University

High School

- West

- Midwest

- Northeast

- Southeast

- Other

- Alaska

- Arizona

- California

- Colorado

- Nevada

- New Mexico

- Northern California

- Oregon

- Southern California Preps

- Washington

- Edgy Tim

- Indiana

- Kansas

- Nebraska

- Iowa

- Michigan

- Minnesota

- Missouri

- Oklahoma Varsity

- Texas Basketball

- Texas

- Wisconsin

- Delaware

- Maryland

- New Jersey Basketball

- New Jersey

- New York City Basketball

- Ohio

- Pennsylvania

- Greater Cincinnati

- Virginia

- West Virginia Preps

ADVERTISEMENT

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Why Doesn't America Have a SOVEREIGN WEALTH FUND?

- Thread starter What Would Jesus Do?

- Start date

And yet they feed the myth of the rugged individualist. They actually have a govt fund based on natural resources. The us govt practically gives those resources away. And once the companies are done exploiting them we let them leave without cleaning up. It’s the corporate way.Alaska residents get something like this.

Why does the US seem ok with letting citizens do without basic healthcare and lodging?United States has bankrupt itself being the police of the world. Maybe somebody else could step up. Or raise taxes to do what you suggest.

So, You are good with fellow citizens doing without.Because at our core we aren’t socialists or communists.

We saw a great social science experiment about this during the pandemic.

The government started sending free money to everyone.

Result? No one wanted to work (especially at the low end of the income scale).

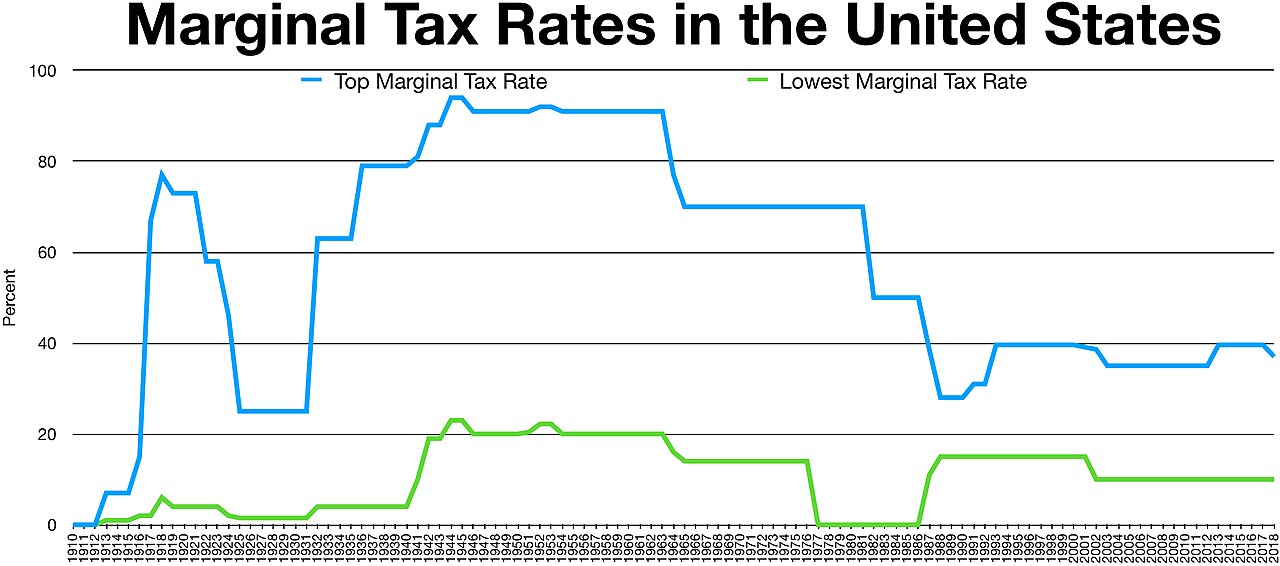

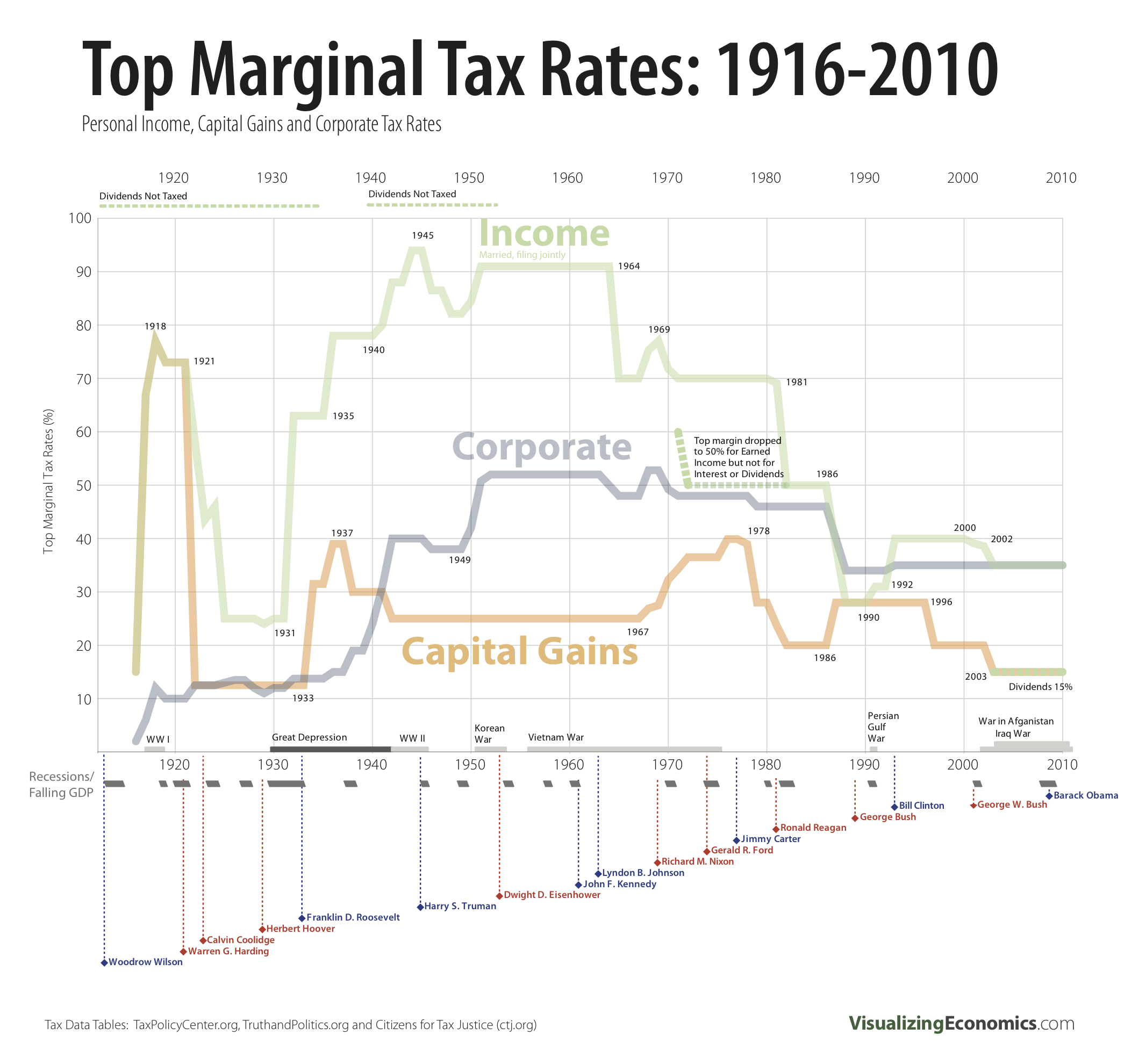

I'd love to see some post WWII tax rates. Everybody pays what they should pay. Of the course the super rich would protest.

Capitalism baby! Let freedom ring!So, You are good with fellow citizens doing without.

Did you read and or understand my post?Because at our core we aren’t socialists or communists.

And, we don’t look out for all citizens. Just the stoopid rich.Because at our core we aren’t socialists or communists.

We are the most philanthropic country in the world, that’s a fact.Did you read and or understand my post?

And, we don’t look out for all citizens. Just the stoopid rich.

Did you read and or understand my post?Because at our core we aren’t socialists or communists.

Your company obviously wanted to pay less than the going rate. You pretended to pay top money. Oh, not enough people were willing to hire into your company. Wonder why?jWe saw a great social science experiment about this during the pandemic.

The government started sending free money to everyone.

Result? No one wanted to work (especially at the low end of the income scale).

Pay the most, provide the best healthcare, have the best retirement… What is your view.?kWe are the most philanthropic country in the world, that’s a fact.

Pay the most, provide the best healthcare, have the best retirement… What is your view.?k

Last edited:

Always struck by the peculiarity of a mindset that confers title to 100% of one’s earnings to the government, and if they take less than 100% considers it the government ‘giving’ you the money…Or give money back to the wealthy…not everyone else.

The Fed made a profit of about $90b in 2020. And then in 2021 it made about $110b. That money and the profit made in the years before that goes to the government and just gets pissed away by politicians. That money belongs to US citizens, it’d be nice if it was held as savings like a wealth fund.

Nowhere are shrunken asset prices more apparent than in the Fed’s own hyper-leveraged balance sheet, which runs at a ratio of assets to equity of more than 200. As of March 31, 2022, the Fed disclosed, deep in its financial statement footnotes, a net mark-to-market (MTM) loss of $330 billion on its investments. Since then, the interest rates on 5 and 10-year Treasury notes are up about an additional one-half percent. With an estimated duration of 5 years on the Fed’s $8 trillion of long-term fixed rate investments in Treasury and mortgage securities, this implies an additional loss of about $200 billion in round numbers, bringing the Fed’s total MTM loss to over $500 billion.The Fed made a profit of about $90b in 2020. And then in 2021 it made about $110b. That money and the profit made in the years before that goes to the government and just gets pissed away by politicians. That money belongs to US citizens, it’d be nice if it was held as savings like a wealth fund.

Compare this $500 billion loss to the Fed’s total capital of $41 billion. The loss is 12 times the Fed’s total capital, rendering the Fed technically insolvent on a mark-to-market basis. Does a MTM insolvency matter for a fiat currency-printing central bank? An interesting question—most economists argue such insolvency is not important, no matter how large. What do you think, candid Reader?

The Fed’s first defense of its huge MTM loss is that the loss is unrealized, so if it hangs on to the securities long enough it will eventually be paid at par. This would be a stronger argument in an unleveraged balance sheet, which did not have the Fed’s $5 trillion of floating rate liabilities. With the Fed’s leverage, however, the unrealized losses suggest that it has operating losses to come, if the higher short-term interest rates implied by current market prices come to pass.

The Fed’s second defense is that it has changed its accounting so that realized losses on securities or operating losses will not affect its reported retained earnings or capital. Instead, the resulting debits will be hidden in a dubious “deferred asset” account. Just change the accounting! (This is exactly what the insolvent savings and loans did in the 1980s, with terrible consequences.)

What fun it is to imagine what any senior Federal Reserve examiner would tell a bank holding company whose MTM losses were 12 times its capital. And what any such examiner would say if the bank proposed to hide realized losses in a “deferred asset” account instead of reducing its capital!

Here is a shorthand way to think about the dynamics of how Fed operating losses would arise from their balance sheet: The Fed has about $8 trillion in long-term, fixed-rate assets. It has about $3 trillion in non-interest-bearing liabilities and capital. Thus, it has a net position of $5 trillion of fixed rate assets funded by floating rate liabilities. (In other words, inside the Fed is the financial equivalent of a giant 1980s savings and loan.)

Given this position, it is easy to see that pro forma, for each 1% rise in short-term interest rates, the Fed’s annual earnings will be reduced by about $50 billion. What short-term interest rate would it take to wipe out the Fed’s profits? The answer is 2.7%. If their deposits and repo borrowings cost 2.7%, the Fed’s profits and its contribution to the U.S. Treasury will be zero. If they cost more than 2.7%, as is called for in the Fed’s own projections, the Fed starts making operating losses.

How big might these losses be? In the Fed staff’s own recent projections, in its most likely case, the projected operating losses add up to $60 billion. This is 150% of the Fed’s total capital. In the pessimistic case, losses total $180 billion, over 4 times its capital, and the Fed makes no payments to the Treasury until 2030.

In such cases, should the Fed’s shareholders, who are the commercial banks, be treated like normal shareholders and have their dividends cut? Or might, as is clearly provided in the Federal Reserve Act, the shareholders be assessed for a share of the losses? These outcomes would certainly be embarrassing for the Fed and would be resisted.

The central bank of Switzerland, the Swiss National Bank (SNB), did pass on its dividends in 2013, after suffering losses. The SNB Chairman gave a speech at the time, saying in effect, “Sorry! But that’s the way it is.” Under its chartering act, the SNB—completely unlike the Fed—must mark its investment portfolio to market in its official profit and loss statement. Accordingly, in 2022 so far, the SNB has reported a net loss of $31 billion for the first quarter and a net loss of $91 billion for the first six months of this year.

Maybe someday we will get a real independent audit of the Federal Reserve. Hoping it is not postmortem.Nowhere are shrunken asset prices more apparent than in the Fed’s own hyper-leveraged balance sheet, which runs at a ratio of assets to equity of more than 200. As of March 31, 2022, the Fed disclosed, deep in its financial statement footnotes, a net mark-to-market (MTM) loss of $330 billion on its investments. Since then, the interest rates on 5 and 10-year Treasury notes are up about an additional one-half percent. With an estimated duration of 5 years on the Fed’s $8 trillion of long-term fixed rate investments in Treasury and mortgage securities, this implies an additional loss of about $200 billion in round numbers, bringing the Fed’s total MTM loss to over $500 billion.

Compare this $500 billion loss to the Fed’s total capital of $41 billion. The loss is 12 times the Fed’s total capital, rendering the Fed technically insolvent on a mark-to-market basis. Does a MTM insolvency matter for a fiat currency-printing central bank? An interesting question—most economists argue such insolvency is not important, no matter how large. What do you think, candid Reader?

The Fed’s first defense of its huge MTM loss is that the loss is unrealized, so if it hangs on to the securities long enough it will eventually be paid at par. This would be a stronger argument in an unleveraged balance sheet, which did not have the Fed’s $5 trillion of floating rate liabilities. With the Fed’s leverage, however, the unrealized losses suggest that it has operating losses to come, if the higher short-term interest rates implied by current market prices come to pass.

The Fed’s second defense is that it has changed its accounting so that realized losses on securities or operating losses will not affect its reported retained earnings or capital. Instead, the resulting debits will be hidden in a dubious “deferred asset” account. Just change the accounting! (This is exactly what the insolvent savings and loans did in the 1980s, with terrible consequences.)

What fun it is to imagine what any senior Federal Reserve examiner would tell a bank holding company whose MTM losses were 12 times its capital. And what any such examiner would say if the bank proposed to hide realized losses in a “deferred asset” account instead of reducing its capital!

Here is a shorthand way to think about the dynamics of how Fed operating losses would arise from their balance sheet: The Fed has about $8 trillion in long-term, fixed-rate assets. It has about $3 trillion in non-interest-bearing liabilities and capital. Thus, it has a net position of $5 trillion of fixed rate assets funded by floating rate liabilities. (In other words, inside the Fed is the financial equivalent of a giant 1980s savings and loan.)

Given this position, it is easy to see that pro forma, for each 1% rise in short-term interest rates, the Fed’s annual earnings will be reduced by about $50 billion. What short-term interest rate would it take to wipe out the Fed’s profits? The answer is 2.7%. If their deposits and repo borrowings cost 2.7%, the Fed’s profits and its contribution to the U.S. Treasury will be zero. If they cost more than 2.7%, as is called for in the Fed’s own projections, the Fed starts making operating losses.

How big might these losses be? In the Fed staff’s own recent projections, in its most likely case, the projected operating losses add up to $60 billion. This is 150% of the Fed’s total capital. In the pessimistic case, losses total $180 billion, over 4 times its capital, and the Fed makes no payments to the Treasury until 2030.

In such cases, should the Fed’s shareholders, who are the commercial banks, be treated like normal shareholders and have their dividends cut? Or might, as is clearly provided in the Federal Reserve Act, the shareholders be assessed for a share of the losses? These outcomes would certainly be embarrassing for the Fed and would be resisted.

The central bank of Switzerland, the Swiss National Bank (SNB), did pass on its dividends in 2013, after suffering losses. The SNB Chairman gave a speech at the time, saying in effect, “Sorry! But that’s the way it is.” Under its chartering act, the SNB—completely unlike the Fed—must mark its investment portfolio to market in its official profit and loss statement. Accordingly, in 2022 so far, the SNB has reported a net loss of $31 billion for the first quarter and a net loss of $91 billion for the first six months of this year.

On the one hand, most of us probably don't like the US being the policeman of the world.United States has bankrupt itself being the police of the world. Maybe somebody else could step up. Or raise taxes to do what you suggest.

On the other hand, do we really want someone else doing it?

And on the 3rd hand, if we are going to play that role, why can't we do a better job of it?

It's not actually policeman 'for the world'.On the one hand, most of us probably don't like the US being the policeman of the world.

On the other hand, do we really want someone else doing it?

And on the 3rd hand, if we are going to play that role, why can't we do a better job of it?

“I spent thirty-three years and four months in active military service, and during that period I spent most of my time being a high-class muscle man for Big Business, for Wall Street and the bankers. In short, I was a racketeer, a gangster for capitalism. I helped make Honduras right for the American fruit companies in 1903. I helped purify Nicaragua for the International Banking House of Brown Brothers in 1902–1912. I helped make Mexico and especially Tampico safe for American oil interests in 1914. I brought light to the Dominican Republic for the American sugar interests in 1916. I helped make Haiti and Cuba a decent place for the National City Bank boys to collect revenues in. I helped in the raping of half a dozen Central American republics for the benefit of Wall Street. In China in 1927 I helped see to it that Standard Oil went on its way unmolested. Looking back on it, I might have given Al Capone a few hints. The best he could do was to operate his racket in three districts. I operated on three continents.”

Last edited:

This comment got me thinking

[Norway] is a major player in the oil and gas industry. All told, Oslo expects to bring in about $109bn from the petroleum sector this year – $82bn more than in 2021. Much of that will go to the country’s sovereign wealth fund, a national nest egg worth more than $1tn.

Depending on how much "more" than $1 trillion it actually is, that approaches $200,000 per citizen.

If the US had a comparable Sovereign Wealth Fund, it would hold over $60 trillion.

Norway is portrayed as both hero and villain in Europe’s energy crisis

Many countries are counting on Norwegian fuel to get them through the winter months, writes Emily Rauhala. But critics call the energy income obscenewww.independent.co.uk

Couple issues.

One is that we are constantly doing the tax cuts thing.

Second of course is they have a bunch of oil to sell and a very small population to care for. Plus their country in terms of land size isn't super huge either.

We have some oil but our population is much larger and quite frankly we use that oil.

The state of North Dakota does this. A percentage of all oil and gas tax revenue goes to a ‘Legacy Fund’. I think the current balance is ~8 billion.

Because we prefer that you maga scum move to russia where you will find out that your fuhrer really does not give a shit for you and only cares about what you can do for him.You are free to move there.

Since libs think just about every country is better than the U.S., I don't understand why they don't just leave.

IIRC, that quote from Gen. Butler is credited with undermining the effort by a group of businessmen to overthrow FDR and make the US a fascist nation.It's not actually policeman 'for the world'.

“I spent thirty-three years and four months in active military service, and during that period I spent most of my time being a high-class muscle man for Big Business, for Wall Street and the bankers. In short, I was a racketeer, a gangster for capitalism. I helped make Honduras right for the American fruit companies in 1903. I helped purify Nicaragua for the International Banking House of Brown Brothers in 1902–1912. I helped make Mexico and especially Tampico safe for American oil interests in 1914. I brought light to the Dominican Republic for the American sugar interests in 1916. I helped make Haiti and Cuba a decent place for the National City Bank boys to collect revenues in. I helped in the raping of half a dozen Central American republics for the benefit of Wall Street. In China in 1927 I helped see to it that Standard Oil went on its way unmolested. Looking back on it, I might have given Al Capone a few hints. The best he could do was to operate his racket in three districts. I operated on three continents.”

Nearly 100 years later, Big Business is more powerful than ever.

Some people prefer it that way. I'm not a fan.

We don't have a revenue problem, we have a spending problem. That problem starts with military spending, and continues into some extremely ridiculous discretionary spending.More likely, I think, because we value tax cuts for the rich over a national savings account for all.

We also think America's natural resources ought to belong to folks like Exxon and Koch rather than to the people of our nation.

I may not approve of how Norway made all that money, but I do approve of how they are handling it.

I'm sure we could agree on a bunch of things to cut - and yes, military spending is top tier.We don't have a revenue problem, we have a spending problem. That problem starts with military spending, and continues into some extremely ridiculous discretionary spending.

But until we cut the bills, we need to pay the bills. Which means raising revenues to do so. And preferably a little more so we can peck away at the national debt.

I'm surprised the national debt isn't getting more attention. Interest on the ND is already a big chunk of the budget. Imagine what that will look like with soaring interest rates.

Some clever person should be able to calculate when interest payments are likely to hit $1 trillion a year.

We need to cut deficit spending in order to pay the bills. Is that better?I'm sure we could agree on a bunch of things to cut - and yes, military spending is top tier.

But until we cut the bills, we need to pay the bills. Which means raising revenues to do so. And preferably a little more so we can peck away at the national debt.

I'm surprised the national debt isn't getting more attention. Interest on the ND is already a big chunk of the budget. Imagine what that will look like with soaring interest rates.

Some clever person should be able to calculate when interest payments are likely to hit $1 trillion a year.

We need to cut the deficitspendingin order to pay the bills. Is that better?

Even better with this small modification.

It's a real problem in relation to new debt and maturing debt. It looks like the average maturity of the debt is 76 months. Of course we will probably have a major recession or depression by then. I would prefer more of an effort to tackle this thru fiscal means, spending reductions. Raise taxes some too, ok, but reduce spending more and get rid of inefficiencies and waste. Anything that doesn't directly benefit people. We spend as much on military as the next 10 countries combined. That seems arbitrary to me. You can't tell me there can't be cuts in other departments, probably no one would notice.I'm sure we could agree on a bunch of things to cut - and yes, military spending is top tier.

But until we cut the bills, we need to pay the bills. Which means raising revenues to do so. And preferably a little more so we can peck away at the national debt.

I'm surprised the national debt isn't getting more attention. Interest on the ND is already a big chunk of the budget. Imagine what that will look like with soaring interest rates.

Some clever person should be able to calculate when interest payments are likely to hit $1 trillion a year.

Last edited:

According to this forecast, just interest payments on the national debt should hit $1 trillion around 2032. Could be sooner if that 10 Year Treasury forecast is too low.I'm sure we could agree on a bunch of things to cut - and yes, military spending is top tier.

But until we cut the bills, we need to pay the bills. Which means raising revenues to do so. And preferably a little more so we can peck away at the national debt.

I'm surprised the national debt isn't getting more attention. Interest on the ND is already a big chunk of the budget. Imagine what that will look like with soaring interest rates.

Some clever person should be able to calculate when interest payments are likely to hit $1 trillion a year.

Interest on the National Debt and How It Affects You

The interest on the national debt is how much the federal government pays on the outstanding public debt. Learn how it's calculated and what it means for you.

Posted last Thursday:Some clever person should be able to calculate when interest payments are likely to hit $1 trillion a year.

In fiscal year 2020, at the height of covid stimulus mania, Congress managed to spend nearly twice what the federal government raised in taxes.

Yet in 2021, with Treasury debt piled sky high and spilling over $30 trillion, Congress was able to service this gargantuan obligation with interest payments of less than $400 billion. The total interest expense of $392 billion for the year represented only about 6 percent of the roughly $6.8 trillion in federal outlays.

...

If Treasury rates continue to rise, and rise precipitously, the effects on congressional budgeting will be immediate and severe. Even if we laughably assume total federal debt remains static at around $23.8 trillion (the publicly held portion of the $30 trillion), interest rates of merely 2 or 3 percent will cause interest expense to rise considerably. Average weighted rates of only 5 percent would cost taxpayers more than $1 trillion every year. Historically, average rates of 7 percent swell that number to more than $1.5 trillion. Rates of 10 percent—hardly unthinkable, given the Paul Volcker era of the late seventies and early eighties—would cause debt service to explode to over $2.3 trillion.

Interest on debt in the hands of the public at different interest rates (billions)

| Total debt in the hands of the public | $23,874. 2 |

| Interest rate | Interest expense |

| 1% | $238.70 |

| 2% | $477.50 |

| 3% | $716.20 |

| 4% | $955.00 |

| 5% | $1,193.70 |

| 6% | $1,432.50 |

| 7% | $1,671.20 |

| 8% | $1,909.90 |

| 9% | $2,148.70 |

| 10% | $2,387.40 |

Again, even 5 percent average rates would cause debt service to become the single biggest annual expenditure for Congress—ahead of Social Security ($1.2 trillion), Medicare ($826 billion), and the Department of Defense ($704 billion). The starting point for budget makers every year would be an interest expense totaling nearly half of realistic tax revenue.

Weak sauce.Some people need an "incentive" to make something more for themselves.

Too much welfare is a "disincentive" to doing that.

A sovereign wealth fund is there for all citizens. It doesn’t choose winners and losers.

Because we have " so many ". Norway has the population of Wisconsin...Why do we have so many doing “without”?

The % does not lie. Our % of those who do without is shameful.Because we have " so many ". Norway has the population of Wisconsin...

Why would we raise taxes when no one is serious about cutting spending? They’ll just blow through more money.I suggest we use half of our Sovereign Wealth Fund to pay off the national debt. Oh wait.

Alternatively, we could restore the tax rates under Reagan.

Thanks.Posted last Thursday:

In fiscal year 2020, at the height of covid stimulus mania, Congress managed to spend nearly twice what the federal government raised in taxes.

Yet in 2021, with Treasury debt piled sky high and spilling over $30 trillion, Congress was able to service this gargantuan obligation with interest payments of less than $400 billion. The total interest expense of $392 billion for the year represented only about 6 percent of the roughly $6.8 trillion in federal outlays.

...

If Treasury rates continue to rise, and rise precipitously, the effects on congressional budgeting will be immediate and severe. Even if we laughably assume total federal debt remains static at around $23.8 trillion (the publicly held portion of the $30 trillion), interest rates of merely 2 or 3 percent will cause interest expense to rise considerably. Average weighted rates of only 5 percent would cost taxpayers more than $1 trillion every year. Historically, average rates of 7 percent swell that number to more than $1.5 trillion. Rates of 10 percent—hardly unthinkable, given the Paul Volcker era of the late seventies and early eighties—would cause debt service to explode to over $2.3 trillion.

Interest on debt in the hands of the public at different interest rates (billions)

Total debt in the hands of the public $23,874. 2 Interest rate Interest expense 1% $238.70 2% $477.50 3% $716.20 4% $955.00 5% $1,193.70 6% $1,432.50 7% $1,671.20 8% $1,909.90 9% $2,148.70 10% $2,387.40

Again, even 5 percent average rates would cause debt service to become the single biggest annual expenditure for Congress—ahead of Social Security ($1.2 trillion), Medicare ($826 billion), and the Department of Defense ($704 billion). The starting point for budget makers every year would be an interest expense totaling nearly half of realistic tax revenue.

That's clearly unsustainable.

Interesting, the lowest federal spending to gdp going back to WW2 was 10% of gdp under Truman in 1948. We had a surplus that year.

"These recommendations would reduce expenditures to 37.1 billion dollars and increase revenues to 38.9 billion dollars. We would then have a budget surplus of 1.8 billion dollars." - Harry S Truman

www.presidency.ucsb.edu

www.presidency.ucsb.edu

"These recommendations would reduce expenditures to 37.1 billion dollars and increase revenues to 38.9 billion dollars. We would then have a budget surplus of 1.8 billion dollars." - Harry S Truman

Annual Budget Message to the Congress: Fiscal Year 1948 | The American Presidency Project

www.presidency.ucsb.edu

If we could ever bring in more than we spend, that might be feasible... as is er have tens of trillions in debt that isn't going away any time soon.This comment got me thinking

[Norway] is a major player in the oil and gas industry. All told, Oslo expects to bring in about $109bn from the petroleum sector this year – $82bn more than in 2021. Much of that will go to the country’s sovereign wealth fund, a national nest egg worth more than $1tn.

Depending on how much "more" than $1 trillion it actually is, that approaches $200,000 per citizen.

If the US had a comparable Sovereign Wealth Fund, it would hold over $60 trillion.

Norway is portrayed as both hero and villain in Europe’s energy crisis

Many countries are counting on Norwegian fuel to get them through the winter months, writes Emily Rauhala. But critics call the energy income obscene

I think, due to the USD current position as reserve currency, that it will be sustained longer than either of us would guess.Thanks.

That's clearly unsustainable.

Similar threads

- Replies

- 0

- Views

- 76

- Replies

- 2

- Views

- 142

- Replies

- 9

- Views

- 170

ADVERTISEMENT

ADVERTISEMENT